Average Home Insurance Costs Across the United States

Let’s talk numbers. Most homeowners across America pay somewhere between $1,700 and $2,200 per year for home insurance. Break that down monthly, and you’re looking at about $140 to $185 for a typical policy with $250,000 in dwelling coverage.

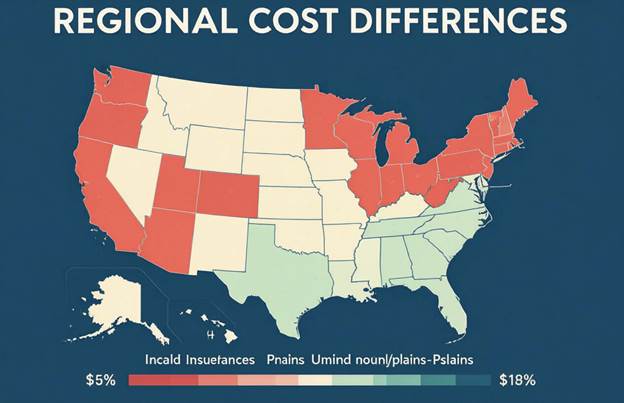

Geography makes a massive difference here. If you live along the coast where hurricanes are a real threat, expect to pay significantly more. Florida homeowners often shell out $3,000 to $4,000 annually, sometimes even higher depending on their specific location. Louisiana and Texas residents face similar premium challenges because of their exposure to severe weather events that regularly damage homes.

But it’s not all expensive news. Oregon, Idaho, and Utah residents often enjoy some of the lowest premiums in the country. These states typically see annual costs under $1,000 to $1,200 for comparable coverage levels.

The difference comes down to risk. Less natural disaster activity means insurers face fewer claims, and those savings get passed along to policyholders.

City versus country matters too. Urban homeowners generally pay higher premiums than their rural counterparts. Why? Replacement costs run higher in cities where labor and materials cost more. Crime rates tend to be elevated in populated areas, and population density itself increases certain risks. Your peaceful farmhouse in Iowa will likely cost less to insure than a comparable home in downtown Chicago.

Key Factors That Determine Your Insurance Premiums

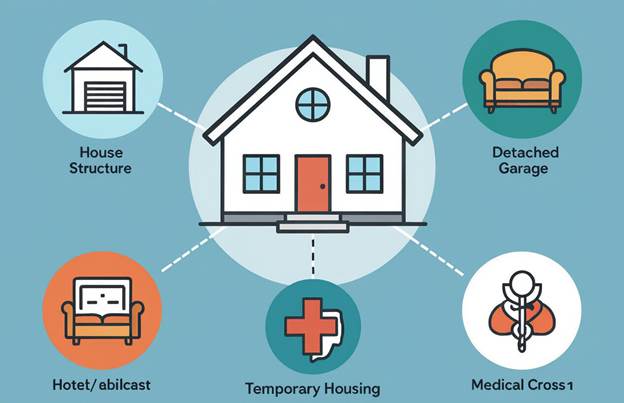

Your home’s physical characteristics play a huge role in what you’ll pay. Age matters a lot. Older homes cost more to insure because aging electrical systems, outdated plumbing, and older roofing materials pose higher risks. Construction type weighs in too. Wood frame houses typically carry higher premiums than brick or concrete structures since they’re more vulnerable to fire damage.

Square footage and replacement cost tie directly to your premium. Bigger homes cost more to rebuild, so they cost more to insure. Simple math there.

Where you live impacts your rates in multiple ways beyond just state boundaries. Insurers look at natural disaster risk zones very carefully. Are you in a tornado alley or wildfire-prone region? Your rates will reflect that exposure. Distance to the nearest fire station and fire hydrants also factors in. Quick emergency response can mean the difference between minor damage and total loss.

Your claims history follows you around like a shadow. File even one claim, and you might see your rates jump 20% to 40% for the next three to seven years. Insurance companies view past claims as predictors of future ones, fair or not.

Personal factors round out the equation. Your credit score influences your premium more than most people realize. Better credit often translates to lower rates because insurers have found correlations between credit responsibility and claim frequency. The coverage amounts you choose, your deductible level, and whether you bundle multiple policies together can swing your premiums by 25% to 50% in either direction.

Proven Strategies to Lower Your Home Insurance Costs

Want to cut your insurance bill?

Raising your deductible is the fastest way. Jump from a $500 deductible to $1,000 or $2,500, and you could see your premium drop 15% to 30%. Just remember that you’ll need to pay that higher amount out of pocket if you file a claim.

Home improvements aren’t just about comfort and aesthetics. Security systems, monitored fire alarms, storm shutters, impact-resistant roofing, and updated electrical or plumbing systems can all earn you discounts ranging from 5% to 20%. Talk to your insurer before making major upgrades to find out which improvements they reward most generously.

Bundling works. Period. Most insurance companies offer 15% to 25% discounts when you purchase both home and auto insurance from them. That savings applies to both policies, making it a win-win situation compared to splitting your business between separate insurers.

Stay claims-free if you possibly can. Every year without a claim builds your value as a low-risk customer. Work on improving your credit score too, since better credit can significantly reduce your costs. Shop around annually because rates change and new discounts appear. Ask about loyalty discounts, professional association memberships, and other special programs you might qualify for.

How to Compare Policies and Choose the Right Insurance Company

Never accept the first quote you receive. Get quotes from at least three to five different insurers and compare everything, not just the bottom line price. Look at coverage limits, deductibles, exclusions, and available endorsement options. A cheaper policy might leave you seriously underinsured when disaster strikes.

Financial strength matters enormously when choosing an insurer. Check ratings from A.M. Best, Standard & Poor’s, or Moody’s. Look for companies with ratings of A or higher. An amazing policy means nothing if the company can’t actually pay your claim when you need them most.

Customer satisfaction tells you how companies treat people during their most stressful moments. Review scores from J.D. Power and check complaint ratios through state insurance department data. Some companies excel at collecting premiums but fall apart when handling claims.

Independent insurance agents can save you time and effort. They represent multiple carriers, giving you access to various options without needing to contact each company individually. Direct insurers and comparison websites work well too, especially if you’re comfortable doing your own research and prefer a self-service approach.

Essential Tips for Maintaining and Updating Your Coverage

Set a calendar reminder to review your policy every single year. Major life events demand immediate attention to your coverage. Did you renovate your kitchen? Add a home office? Buy expensive jewelry or electronics? Market values change too. Your coverage needs to keep pace with all these shifts.

Document everything you own right now. Take photos and videos of every room, your belongings, serial numbers on electronics, and anything valuable. Keep receipts organized. Store all this information in cloud storage or somewhere off-site. When disaster strikes, you won’t have time to recreate this inventory, and it makes the claims process so much smoother.

Understand the critical difference between replacement cost and actual cash value coverage. Replacement cost pays to rebuild or replace your property without deducting for depreciation. Actual cash value subtracts depreciation based on age and wear. That ten-year-old roof might cost $15,000 to replace, but actual cash value might only pay $7,000 after depreciation. Know which one your policy provides.

Construction costs have exploded recently, jumping 20% to 40% over the past few years. Inflation protection or guaranteed replacement cost endorsements help ensure your coverage keeps pace with these rising costs. Without these protections, you might discover your $250,000 dwelling coverage no longer covers the $320,000 it actually costs to rebuild your home. Check these endorsement options with your insurer to avoid nasty surprises when you need your coverage most.

Leave a Reply